Breathe Easy Again: Consolidation of Debt is a Winning Solution!

Consolidation of debt involves taking multiple debts and combining them into a single, larger loan or credit account. The goal of consolidation is typically to simplify your monthly payments, lower your interest rates, or both. Here are ten quick ways to consolidate debt:

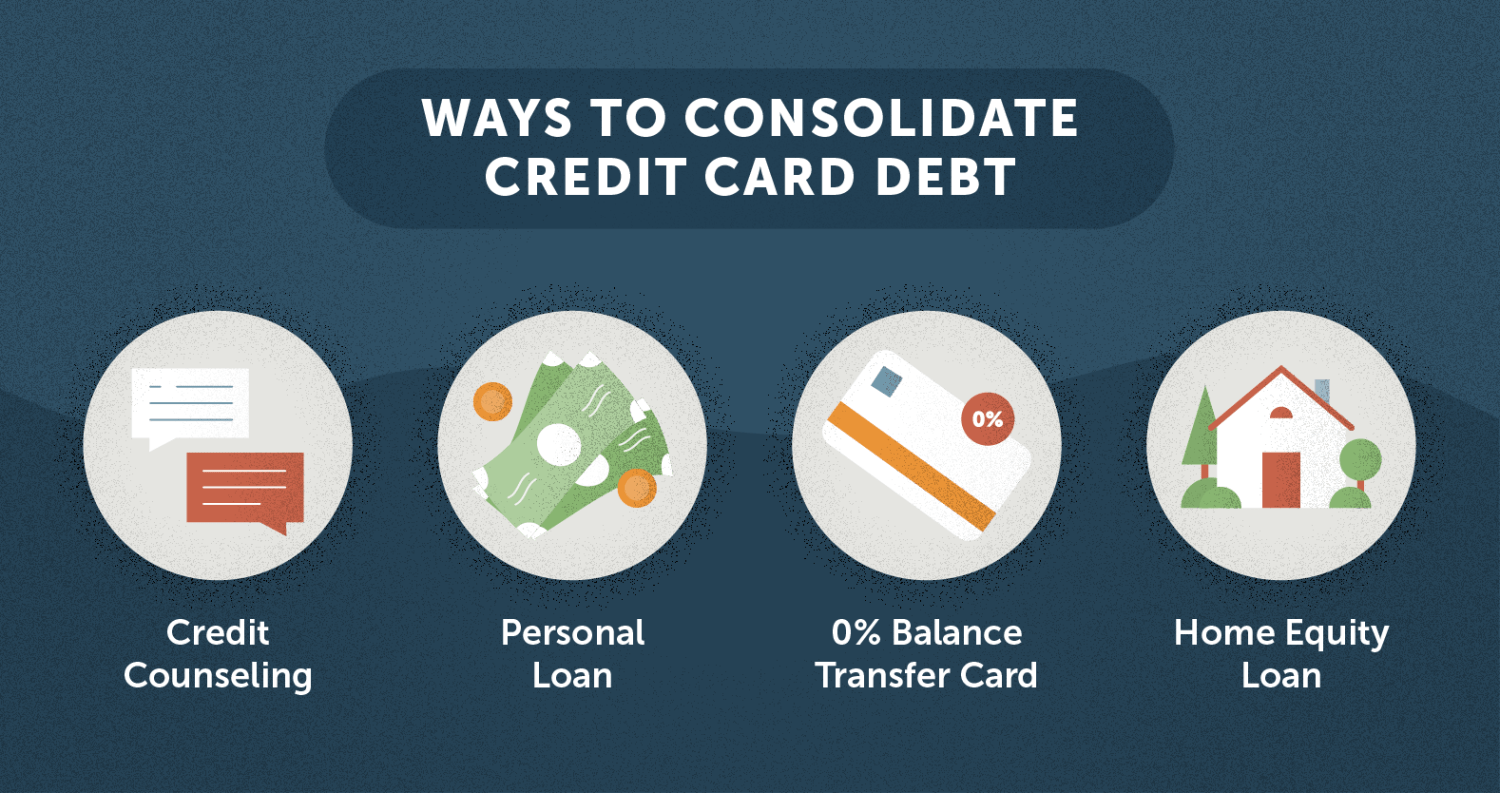

Balance transfer credit cards: If you have multiple high-interest credit card debts, you may be able to transfer them to a new credit card with a 0% introductory APR. This allows you to pay off the balance interest-free for a limited time, typically 12 to 18 months. Keep in mind that there is usually a balance transfer fee, and if you don’t pay off the balance before the promotional period ends, you may end up with a higher interest rate than you started with.

Personal loans: You can take out a personal loan to consolidate multiple debts. This can be a good option if you have a good credit score and can qualify for a low-interest loan. Keep in mind that you will need to make monthly payments on the loan, so be sure you can afford the payments before taking out the loan.

Home equity loans: If you own a home, you may be able to take out a home equity loan to consolidate your debts. A home equity loan allows you to borrow against the equity in your home, and often has a lower interest rate than other types of loans. However, if you default on the loan, you risk losing your home.

Retirement account loans: If you have a 401(k) or other retirement account, you may be able to borrow against it to consolidate your debts. This can be a risky option, as you are essentially borrowing from your future self, and if you leave your job, you may be required to pay back the loan immediately.

Debt management plans: A debt management plan is a type of repayment plan that is set up by a credit counseling agency. The agency will work with your creditors to negotiate lower interest rates and a more manageable payment plan. You will make one monthly payment to the agency, and they will distribute the funds to your creditors.

Debt settlement: Debt settlement involves negotiating with your creditors to settle your debts for less than what you owe. This can be a risky option, as it can damage your credit score and there are no guarantees that your creditors will agree to a settlement.

Peer-to-peer lending: Peer-to-peer lending involves borrowing money from individuals rather than banks or other financial institutions. This can be a good option if you have a good credit score and can qualify for a low-interest loan.

Credit counseling: Credit counseling involves working with a counselor to create a budget and develop a plan for paying off your debts. The counselor can also provide advice on how to improve your credit score and manage your finances.

Debt consolidation companies: Debt consolidation companies are companies that specialize in consolidating debt. They will work with your creditors to negotiate lower interest rates and consolidate your debts into a single loan or credit account.

Cash-out refinancing: If you own a home, you may be able to refinance your mortgage and take out some of the equity in your home to pay off your debts. This can be a good option if you have a good credit score and can qualify for a lower interest rate than your current mortgage.

When considering debt consolidation options, it’s important to do your research and understand the pros and cons of each option. At Donalson Value Partners we’re happy to answer any questions you may have. Make sure you understand the fees, interest rates, and repayment terms before making a decision. It’s also important to remember that debt consolidation is not a magic solution to debt problems – it’s just one tool in a larger financial toolbox. To truly get out of debt, you may need to make changes to your spending habits and lifestyle.