Debt can be a heavy burden that affects various aspects of our lives, from our financial well-being to our mental and emotional health. However, with careful planning and determination, it is possible to erase debt and regain control of your financial future. In this article, our debt-relief experts at Donalson Value Partners will explore with you practical steps and strategies to help you tackle your debts and pave the way towards a debt-free life.

Assess Your Debt: The first step towards debt relief is to have a clear understanding of your debts. Make a list of all your debts, including credit card balances, loans, and any other outstanding obligations. Take note of the interest rates, minimum payments, and due dates for each debt. This will help you get a comprehensive overview of your debts and prioritize them based on urgency and interest rates.

Create a Budget: A budget is a powerful tool that can help you manage your finances effectively and allocate funds towards debt repayment. Calculate your monthly income and expenses to determine how much money you can allocate towards debt repayment. Cut down on unnecessary expenses and prioritize debt payments to accelerate your debt payoff journey.

Negotiate with Creditors: Don’t be afraid to reach out to your creditors and negotiate for better terms. This is exactly what Donalson Value Partners can do for you! You may be able to lower interest rates, negotiate a reduced settlement amount, or obtain a more favorable repayment plan. Many creditors are willing to work with you if you communicate openly and show a genuine commitment to repay your debts.

Prioritize High-Interest Debts: High-interest debts, such as credit card balances, can quickly accumulate and become a significant financial burden. Prioritize paying off high-interest debts first to minimize the overall interest costs. Consider using the “debt avalanche” method, where you pay off debts with the highest interest rates first, while making minimum payments on other debts. This approach can help you save money in the long run and accelerate your debt payoff journey.

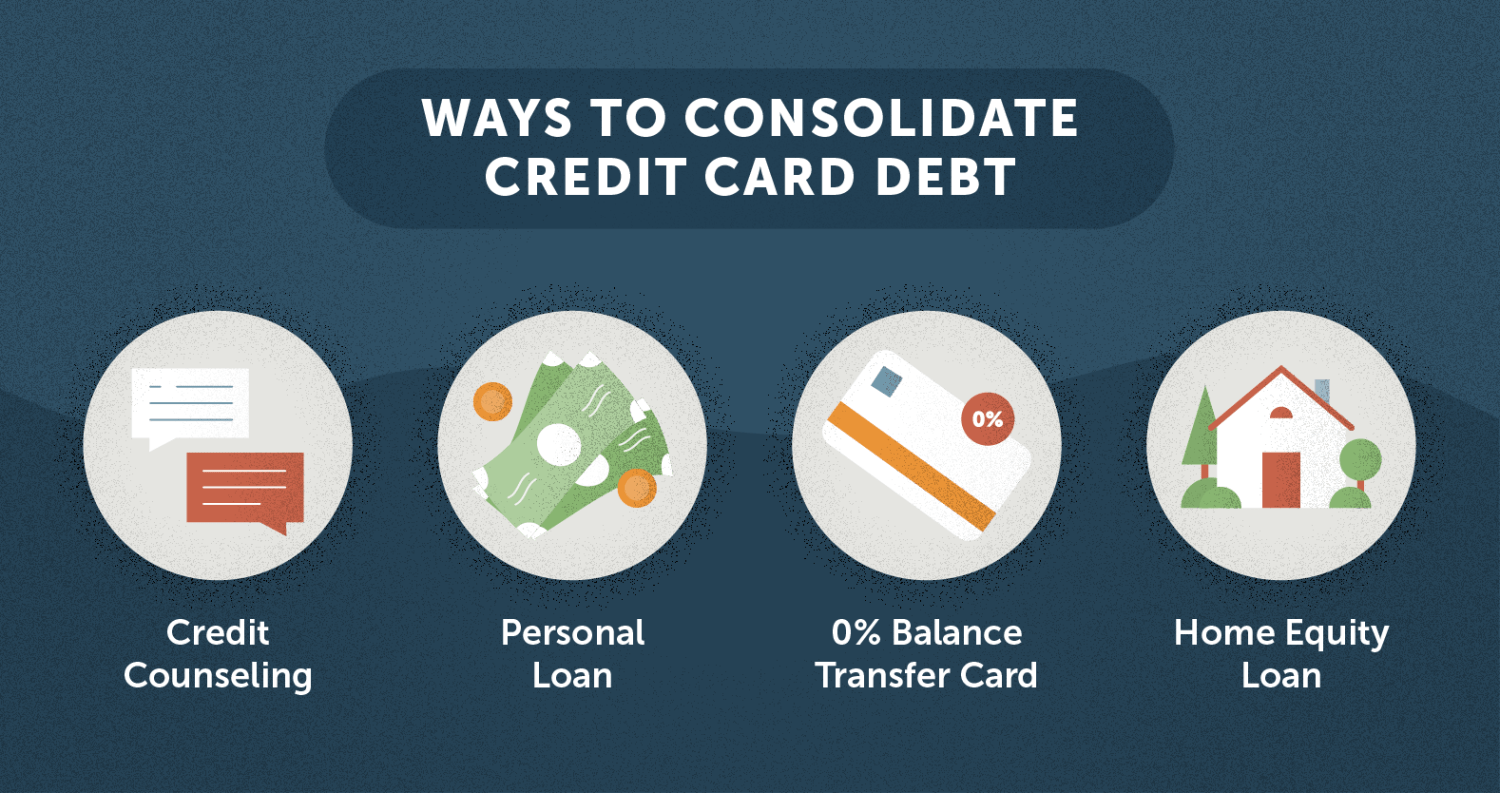

Explore Debt Consolidation or Refinancing Options: If you have multiple debts with high-interest rates, you may consider consolidating your debts into a single loan with a lower interest rate. Debt consolidation or refinancing can simplify your monthly payments and potentially lower your overall interest costs. However, carefully research and compare the terms and fees of different consolidation or refinancing options to ensure they are beneficial for your unique financial situation.

Increase Your Income: Another effective strategy for erasing debt is to boost your income. Look for ways to increase your earnings, such as taking on a side job, freelancing, or selling unwanted items. Use the extra income to make additional payments towards your debts, which can help you pay off your debts faster.

Seek Professional Help: If you are struggling with overwhelming debts, consider seeking professional help from a reputable credit counseling agency, like Donalson Value Partners or a financial advisor. They can provide personalized advice and guidance on how to manage your debts effectively, negotiate with creditors, and develop a customized debt repayment plan.

In conclusion, erasing debt requires careful planning, disciplined budgeting, and persistent effort. By assessing your debts, creating a budget, negotiating with creditors, prioritizing high-interest debts, exploring consolidation or refinancing options, increasing your income, and seeking professional help if needed, you can take proactive steps towards achieving debt relief and securing a brighter financial future. Remember, with determination and a strategic approach, it is possible to erase debt and regain control of your financial well-being.